ACV is actual cost value and means that in case of a claim the insurance carrier will payout based on a roof schedule or depreciated value, less your deductible. RC or replacement cost means the carrier will payout the total cost to replace your damaged roof, less your deductible. Which means, RC will almost always be a better option, when available. However, the up front premium cost may not be ideal, so lets look at some examples.

The general trend is for homeowner insurance policies to only offer ACV on roofs once they get to 10 years old and some carriers even when they are only 5 years old. A newer roof generally means a lower deductible for replacement cost and a lower premium.

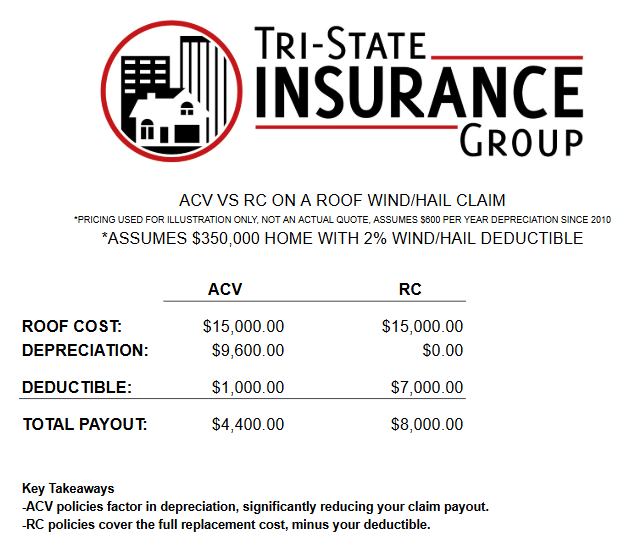

In this example, lets assume we are insuring a home with a coverage limit of $350,000, which is the cost to rebuild the home as it stands now. The roof itself is an architectural shingle, installed in 2010 or 16 years old. To replace that same roof now would cost an estimated $15,000. Insurance carriers will typicaly depreciate the roof about $600 per year. One carrier is offering a low $1,000 deductible, but only ACV coverage on the roof, the other carrier is offering full replacement cost, but a much higher percentage based deductible of 2%. Let’s look at how this price breaks down, when it comes to claim time.

Carrier 1 with a $1,000 deductible will depreciate the value of the roof by $600 per year or $9,600. Carrier 2 offering replacement cost won’t depreciate the replacement cost of the roof at all. Next we need to consider the deductibles, Carrier 1 is much lower at $1000 and Carrier 2 deductible will be $7,000 based on a 2% wind/hail claim deductible. This means that the total payout for Carrier 1 will be $4,400 and Carrier 2 will payout $8,000! That’s $3,600 more compensation with Carrier 2 by going with replacement cost coverage.

Below is a graphic showing this math and how taking the higher wind and hail deductible can net you more compensation.

As you can see, although the higher deductible seems like a bad decision up front, the older your roof is, the more savings a higher deductible can provide. It’s always important to review with your homeowners insurance agent, discuss the ages of your roof and expectation come claim time.

Live in Indiana, Kentucky, or Illinois? If you do, give me a call or email, I’m happy to review or assist you in making the right decision when protecting your most valuable assets.